Ex-Cred execs plead guilty to wire fraud over $150M crypto collapse

Two former executives of the bankrupt crypto lending service Cred have pleaded guilty to wire fraud connected to the company’s collapse.

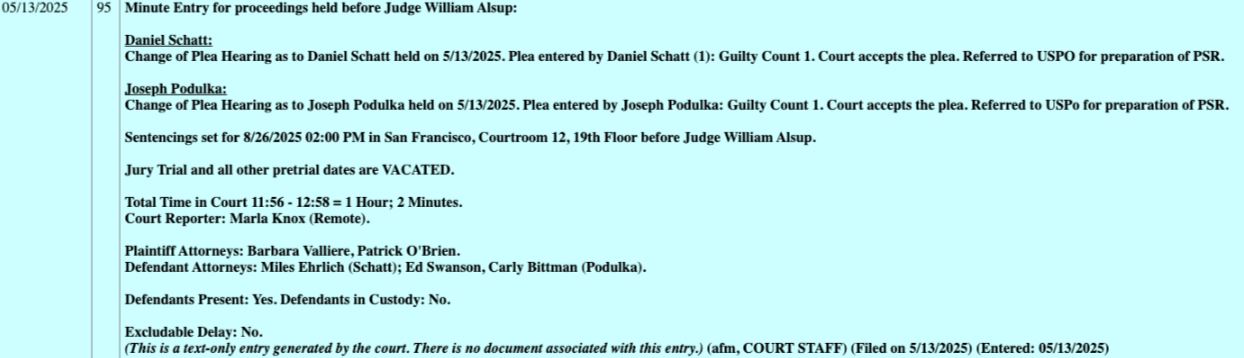

Former Cred CEO Daniel Schatt and chief financial officer Joseph Podulka admitted to wire fraud as part of a plea deal with prosecutors, according to a May 13 text filing in a California District Court.

District Judge William Alsup accepted the plea deals and set a sentencing hearing for Aug. 26. Wire fraud can carry up to 20 years in prison and $250,000 in fines for individuals and $500,00 for businesses.

Law360 reported that as part of the plea agreement, Schatt and Podulka admitted to selectively presenting positive “information [while] failing to disclose negative news” as part of a plan to “induce customers to lend their US currency and digital currencies to Cred.”

Federal prosecutors have reportedly submitted a possible sentence range of up to 72 months for Schatt and up to 62 months for Podulka. Schatt and Podulka were facing 13 charges of wire fraud and money laundering.

Cred customer losses exceed $150 million

When Cred collapsed and filed for bankruptcy, its customers suffered losses of up to $150 million, but the US Department of Justice said in May 2024 that the assets had since climbed to a market value exceeding $783 million.

In the plea agreement, the defendants agreed that their actions led to losses of between $65 million and $150 million for users.

Former Cred chief commercial officer James Alexander was also hit with wire fraud and money laundering charges.

Prosecutors alleged that the Cred executives misled customers about Cred’s lending and investment practices and didn’t disclose that its loan book relied heavily on the Chinese firm MoKredit, which made unsecured microloans to Chinese gamers.

Cred also allegedly claimed to only engage in collateralized lending, and all its crypto investments were hedged, which prosecutors say was false.

After the price of Bitcoin (BTC) dropped by 40% on March 11, 2020, Cred could not meet its margin calls and neared insolvency, and the three executives sought out new customers while downplaying the risks, prosecutors claimed.

When Cred declared bankruptcy in November 2020, numerous users turned to social media to voice concerns and ask if their funds were safe.

Related: Uphold exchange denies owing millions to failed crypto lender Cred

Other crypto founders have also faced legal consequences this year. Alex Mashinsky, the founder and former CEO of bankrupt crypto lending platform Celsius, was sentenced to 12 years in prison for fraud on May 8.

Meanwhile, Wolf Capital co-founder and head trader Travis Ford pleaded guilty on Jan. 10 to wire fraud conspiracy charges for his role in raising over $9 million from investors with false promises of high returns.

Magazine: ChatGPT a ‘schizophrenia-seeking missile,’ AI scientists prep for 50% deaths: AI Eye